Almost every taxpayer who has filed all the required returns and is in a state to prove financial hardship may qualify.

Updated Mar 2, 2026

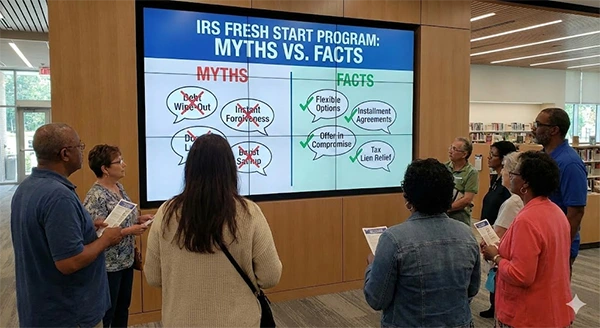

IRS Fresh Start Program: Myths and Facts Every Taxpayer Should Know

“It’s strange that most Americans fear an IRS letter more than a medical diagnosis – and yet, this overlooked program has quietly helped millions to escape tax debt without ruining their finances”.

IRS feels like a flashing danger light on your dashboard – you know something is wrong, but aren’t sure how expensive it can be. That’s exactly why the IRS programme was created : to provide a realistic path out of debt.

“Even the updated IRS now allows an installment agreement for taxpayers owing upto $50,000 – up from the previous lower limits”. (Source – Forbes)

But over time, many myths have piled up around it, making people either take it as a magic wound or a hopeless maze.

Move forward with this guide that clears the misconceptions and what the IRS Fresh Start programme actually offers – and what it doesn’t. Also, visit TaxLawAdvocates.com to get expert answers in one free call.

What does the IRS Fresh Start Program Actually Offer?

The IRS program is a toolkit that makes repayment easier and less damaging. Launched in 2011, its goal was simple – to help the taxpayers who were drowning, not dodging.

It includes:

- Installment agreements (monthly payment plans)

- Offers a compromise (OIC) – a settlement option if you truly can’t afford the full amount.

- Tax lien relief.

- Penalty abatement.

The official IRS site has also provided a lot of information on it, but still misunderstandings exist. Let’s break down the major myths:

Myth #1: The IRS Forgives Tax Debt for Everyone

Fact – The Fresh Start program doesn’t offer blanket forgiveness: “You get debt relief! You get debt relief!”

Debt reduction through the offer in compromise is possible, but only when you genuinely can’t pay – even after liquidating what you own. IRS data says that the agency only accepts a fraction of OIC applications each year.

Real World Instance

If you owe $40,000 but have a steady job, savings and assets – the IRS accepts you to pay. But if you’re unemployed and barely manage essentials, your case might qualify.

Myth #2: You Can Qualify Without Documentation

FACT: If the IRS has a motto, it might be – “If you can’t prove it, it doesn’t count”.

Missing paperwork is the major reason OICs get delayed or rejected. You need to submit your income, expenses, assets and liabilities.

IRS official guidance on Offer in Compromise typically includes these documents:

- Pay stubs

- Bank statements

- Rent/ Mortgage details

- Medical bills

- Business revenue records

Myth #3: It Damages Your Credit Score

FACT: Applying for a fresh start program has no connection with your credit score.

This confusion came from tax liens. After the fresh start expansion, the IRS made it easier to avoid liens and even withdraw them once taxpayers entered qualifying installment agreements.

It’s like a gym membership – signing up won’t make you stronger, but missing payments will for sure hurt you.

Same is the fresh start: application = safe and defaulting = risky.

Myth #4: You Can Handle It Alone with Online Tools

FACT: It may work, but chances are very rare.

The IRS website provides calculators and forms – but it’s like assembling furniture without interest – possible but stressful and every mistake has the potential to fall things apart.

Common issues that come forward while doing it on your own:

- Overreporting time (which can act as a clue for the IRS that you can pay more).

- Missing deductible expenses.

- Misjudging asset values.

- Incorrectly filling out the 656 form (OIC application).

Professional advice can smooth the process – the IRS itself advises that OIC forms are complex, and every error can delay your application.

Myth #5: The Program Is Only for Individuals

FACT: Fresh Start rules apply to both individuals and small businesses – especially those who are struggling with payroll taxes.

Business owners often believe that the IRS is stricter for companies. Yes, payroll tax issues are considered well, but repayment plans and penalty relief are also available.

Businesses that fell behind during downturns, staffing changes, or cash flow crunches commonly qualify.

Conclusion

The IRS Fresh Start program is neither a magic eraser nor a last resort punishment – it’s a structured path to regain control. But figuring out the right path is like driving through fog – possible, but risky.

When misinformations are replaced with facts, the program becomes what it was intended to be: relief, clarity, and a chance to reset.

If you’re not sure about eligibility or required documentation, visit the official IRS website or speak with a qualified tax professional who can help you avoid costly mistakes.

Author - Dushyant K

Finance Writer

Table of Contents

Related Posts