Navigating Debt Repayment Solutions: What You Need to Know

Do you often feel overwhelmed with loans or some other financial obligations you have? Well, you’re not alone, my friend. Managing debts has always been a big concern in society, affecting millions of people across the planet.

In fact, the figure is so big that according to the recent report on the ascent, an American household carries $17.796 trillion of debt by Q2 2024, which averages down to $104,215 per household.

These striking statistics clearly depict the ongoing difficulty many individuals are facing nowadays when it comes to managing or repaying their debts.

But you know what, there are a range of options that can help you navigate towards financial security and overall peace of mind. So, in this read, I will assist you with some practical solutions that can help you address this complicated debt situation.

Let’s start!

Exploring Formal Debt Relief Options

When financial obligations become too challenging to manage, exploring formal debt relief measures can provide a strategic solution. For example, if you reside in Canada, there are specific debt relief options available, such as a consumer proposal to help manage fiscal challenges.

This legally binding agreement, facilitated by a licensed insolvency trustee, allows you to repay creditors a portion of what you owe over up to five years. Once agreed upon, interest on your debts stops, and you retain your assets.

This option serves as an alternative to bankruptcy, providing a less severe impact on your credit score. It also allows for more manageable monthly payments, tailored to your financial situation, ensuring that loan repayment does not hinder your basic living expenses.

Assessing Debt Consolidation Loans

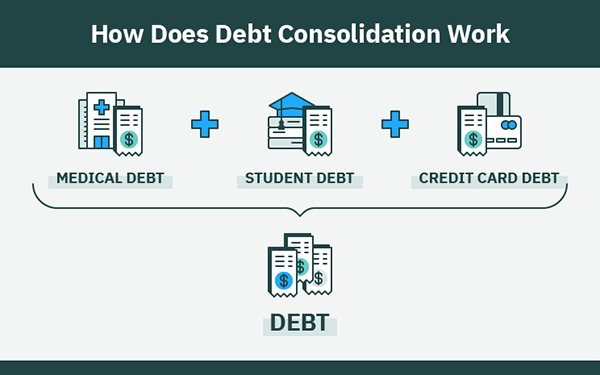

Debt consolidation loans consolidate several debts into one loan, typically at a reduced interest rate. This streamlines your payment process and can decrease the total interest paid throughout the loan. It is crucial to review the conditions of these loans to confirm that the interest rate is effectively lower than what you are currently paying.

Also, evaluate your financial behaviours to avoid incurring new ones after consolidation, which could worsen your fiscal state. A thorough review of your long-term financial objectives and present income stability is critical before deciding on a consolidation loan.

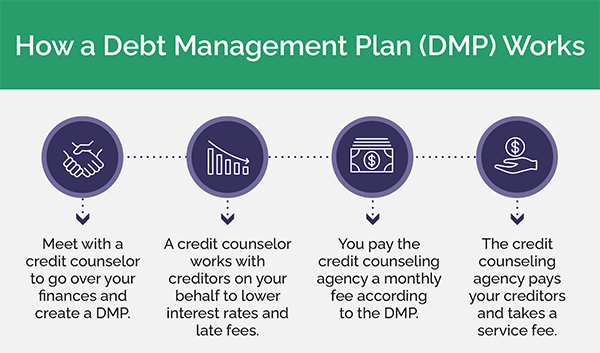

Exploring Debt Management Plans

Credit counseling agencies often facilitate debt management plans (DMPs). A DMP allows you to cover your debts by making monthly payments to them instead of your creditors directly, leading to lower interest rates and forgiven fees in some cases.

On top of that, it also offers a defined repayment schedule that can assist in projecting your financial recovery. Although, these plans typically exclude secured payments such as mortgages or auto loans.

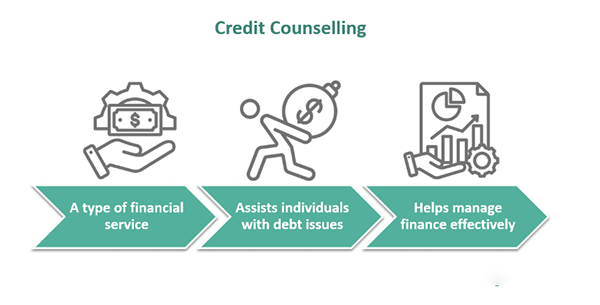

Credit Counseling Services

Credit counselling services provide advice and assistance with managing finances and debts, budget creation assistance, and often offer educational materials and workshops at no cost.

With experienced financial assessment professionals on staff, counsellors will help identify the most appropriate approach to take for your situation, whether that involves developing a DMP or simply improving money management techniques.

Utilizing these services can also lead to healthier spending behaviours and prevent future economic problems. Early involvement with these services can avert severe actions like bankruptcy.

Do You Know?

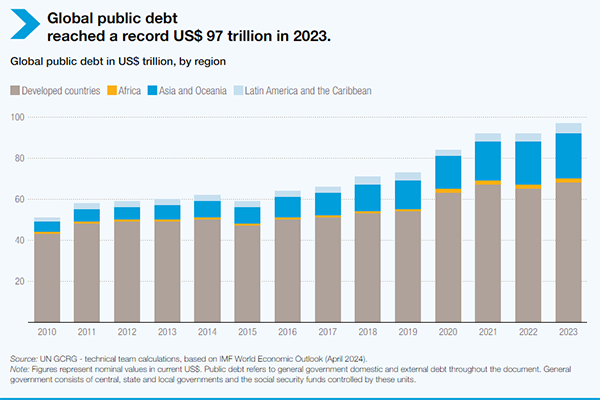

According to the IMF World Economic Outlook of April 2024, the global public debt has reached a record high of US$ 97 trillion in 2023. But it is still one-third of the total in developing countries, which is about US$ 29 trillion.

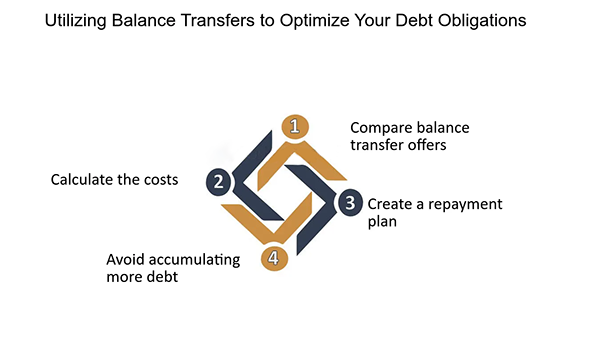

Utilizing Balance Transfers

Balance transfers provide one method for dealing with credit card debt by moving it from cards with higher interest rates to those offering a reduced rate, often as part of promotional deals by card issuers.

Before engaging in such a transfer, however, be mindful that fees may apply and that its effects may only last briefly. Ensure that the transfer costs do not outweigh the savings on interest, and aim to clear the balance before the promotional term concludes. This approach works best when paired with a strict budgeting strategy that prevents accruing additional debt.

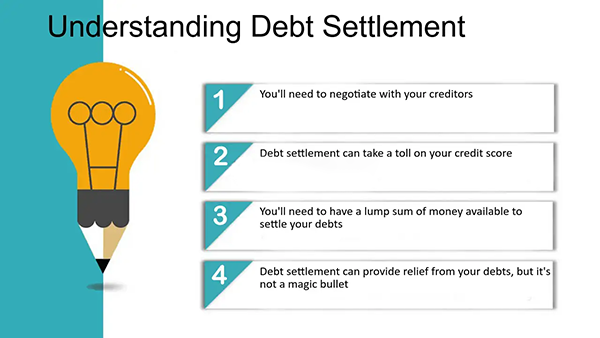

Settling Debts for Less Than You Owe

Debt settlement entails discussions with creditors to agree on a payment that is lower than the full amount owed. This approach can decrease your total debt, but it could notably affect your credit rating and include additional costs.

Opting for this method, it is wise to collaborate with a trusted agency that can handle negotiations for you and clarify possible outcomes. It is also essential to prepare for the tax responsibilities associated with forgiven debt, as the IRS may view settled debts as taxable income.

Conclusion

Debts can be a heavy burden that can significantly disrupt one’s economic situation. But there are a range of solutions available that can help you regain full control of your finances.

And, each solution that is mentioned in this read, whether it’s about formal debt relief or even utilizing the balance transfer, has its own pros and downsides, which are again tailored to different economic situations. So, by having a deep understanding of each solution, you can build a well-informed strategy to manage your debts.