Understanding Ground-Up Construction Loans and Their Benefits

If you’re thinking of constructing your dream house or investing in construction, a ground-up construction loan is what you need.

This is a fund allotted to a real-estate developer planning to build a property from scratch which along with the cost of construction materials involves manpower costs.

In fact, 15% of the rented equipment is used for individual construction today showing how prevalent and crucial these loans are (Source: BigRentz, 2024).

So, in this blog, we will discuss the benefits, requirements, and procedures that you should follow to acquire your construction loan to ensure your project has the best start and end.

It is basically an ideal solution for real estate investors seeking financial support to construct a property on an undeveloped site.

Unlike traditional mortgages that cover existing properties, ground-up construction loans are customized to cover the entire scope of a new building.

This includes the purchase of land, acquiring the necessary permits, paying for labor, and purchasing materials.

With that in mind, these loans are approved and paid out in stages which is better known as ‘draws’, once certain construction requirements have been fulfilled.

Key Features of Ground-Up Construction Loans

Ground-up loans enable the owner to single-handedly cover the entire cost of construction.

Such as purchasing land and paying for the remaining components needed to complete the construction.

Ground-up loans further have the following features:

Initially, the draw ratio will be lower such as when purchasing land or when working on the structure of the site. The finished construction site will cover the draws such as – construction of the foundation, framing of the construction site, and other final elements required. Construction-based staged disbursement does reduce financial risks for lenders as they hold greater control over the funds allocated for the project.

Interest-Only Payments During Construction

During the initial phases of the project, the loan period can be a costly affair as borrowers are only required to make Interest-Only payments during the construction period.

However, when once the construction is finalized, the mortgage can either be transitioned into a conventional one or paid off via other means.

Customizable Loan Terms

As every project has its own characteristics and requirements, the ground-up construction loans are project-centered accordingly.

For such loans, the amount, rate of interest, and repayment are set in accordance with the diversity and weights of the borrower’s profile.

Higher Interest Rates

Construction projects are considered relatively risky, and that’s the reason such loans usually have higher interest rates than traditional mortgages.

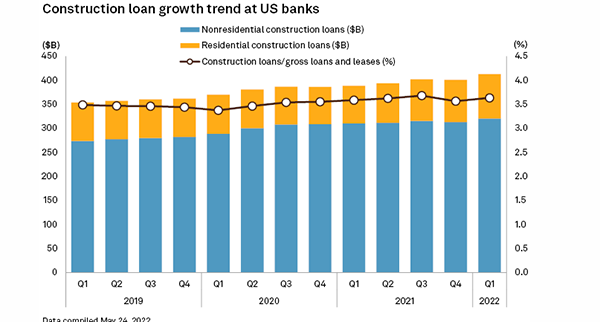

Take a look at the graph below showcasing the growth of the construction loan trend at US Bank.

Eligibility Requirements for Ground-Up Construction Loans

As part of their financial strategy, borrowers must meet certain criteria to get a construction loan such as:

Creditworthiness: Keeping a good credit score matters as it will help you in getting the loan.

Practically, lenders will have more confidence in giving out loans to persons who have a good financial track record.

Experience: Working with a professional contractor or construction manager will add weight to the authenticity of the project and ensure the lenders that the construction activities will be done well.

Detailed Construction Plan: A detailed project plan may also be effective in increasing the chances of loan approval.

Equity contribution: You also need to make an initial payment as a part of the down payment on a loan.

This will picture your commitment and can lead to better loan terms like lower interest rates or more flexible repayment options.

For gaining good levels of approval, these factors are vital in ensuring that the entire course of gaining a ground-construction loan happens without any complications.

Benefits of Ground-Up Construction Loans

Building a new home requires a lot of money so one of the best options for the client can be a ground-up construction loan.

Here are the advantages:

Provides Tailored Financing for Custom Projects

A ground-up construction loan is a perfect fit for real estate developers seeking customized financing be it including building a single-family house, or a multi-unit commercial structure.

Funds Available When You Need Them

The draw schedule guarantees the disbursement of cash when required, such as during the achievement of construction targets.

This would help prevent the squandering of funds and keep the project in a healthy financial condition.

Build Equity from the Start

With the ability to build a property from the ground all the way to the last brick, developers already have equity in the building, unlike when purchasing an already existing property.

This creates an excellent return on investment as once the project is finished, the property may be worth much more than the construction cost.

Improved Cash Flow Management

During the construction phase of the property, the owner is only obligated to pay the interest which greatly reduces the initial economic burden and permits some valuable time.

Improved Design Control

Real estate developers have the freedom to construct and design the building in the manner that they prefer using the funds allocated from a ground-up construction loan.

How to Secure a Ground-Up Construction Loan

Securing a ground-up construction loan might seem daunting to you, however, with a solid framework, it can easily be possible.

Here’s how –

Develop aComprehensivePlan

It will be great if you properly prepare and submit a comprehensive construction plan containing details like architectural plans, budgets, contractor details, and expected time frames when applying for the loan.

Choose the Right Lender

Do bear in mind that not all lenders are highly experienced in terms of financing, therefore, you must look for one who has the proper knowledge in this field.

PrepareYour Financial Documents

To initiate the approval process, lenders will typically ask for your income proof, credit reports, financial statements, and tax returns as additional documentation.

You must collate all this relevant information ahead of time to smoothly streamline this process.

ShowYourExperience

Having experience in constructing projects in the past is highly preferred when you’re aiming to secure a loan for a real estate venture.

It acts as a justification to be confident in your capabilities of managing such a strenuous task.

Common Challenges and How to Overcome Them

As you may have gone through the features and benefits of a ground-up construction loan, there are also a few common challenges you may face when proceeding with it.

But don’t worry as in this section along with the insights of typical setbacks, we have also provided a solution to overcome them.

Cost Overruns

If you take into consideration the amount of resources such as the labor and raw materials, then constructing a building from scratch will definitely be more expensive than just renovations.

Solution: One of the many ways to solve this issue is to first figure out the cost that might be needed to complete the project, and then avoid all those expenses that seem to go overboard.

Delays in Construction

From the inception to construction, there is always a time span of around 6-12 months of planning to be done before a project can come to fruition.

Solution – What you can do here is – analyze the clients’ future demands, cooperate with stakeholders, and employ advanced technologies such as BIM, and dynamic scheduling to counter unforeseen changes.

Meeting Loan Requirements

There can be many circumstances where you may fail to meet the requirements for acquiring a ground construction loan such as your low credit score, or unstable employment.

Also, if you don’t have proper documentation of the ownership of the land, or if the design of the construction is irrelevant or complex.

Solution – A ground construction loan is needed to let your construction projects run smoothly without having massive setbacks.

All you need to do is maintain your credit score, proper papers for the ownership of the land, and definitely a stable job.