After establishing my business, I was all fired up and thrilled but it didn’t take long for me to realize that money management is a different ball game altogether.

As a matter of fact, 82 % of businesses go under because of money mismanagement (Source: Entrepreneur, 2021), and let me tell you that I was close to being one of them.

I was caught up in cash flow errors, buying unnecessary things, and mixing business-related expenses with personal ones.

Almost every single one of these blunders could have ruined me, however, I moved on from those errors, and this time, my purpose is to assist you in not making those errors.

Thus, the following are some of the most common financial mistakes that business owners make with their companies and that you must avoid.

1. Operating Without a Clear Budget Hurts Your Business

When I launched my business, I did not see much value in a budget until reality hit me.

Without specific budget planning, I ended up spending more than I planned and was not able to keep track of my expenses, which created problems in cash flow.

I was left in a situation where I could not bear unexpected expenditures and at the same time, I was unable to allocate funds wisely.

Today, now that I have built up everything by setting a clear budget, I’m able to monitor my expenditures, prevent unproductive spending, and steer my business on the right course.

Indeed it’s simply one of the best tools in minimizing the loss of resources and the stress that comes with running a business.

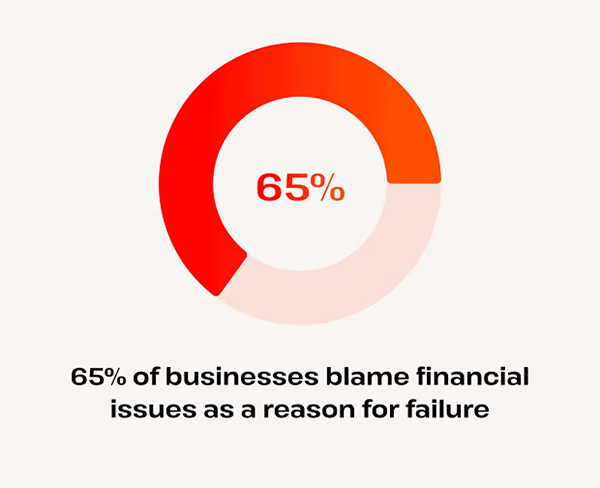

As shown in the pie below, a significant percentage of business owners cite financial issues as the primary reason for their business failures.

2. Failing to Understand Business Finance Leads to Cash Flow Issues

At the first stage of my business career, I did not pay enough attention to managing my financial resources, estimating possible revenues, or monitoring my managerial performance, and this carelessness later became nerve-racking.

However, as soon as I started putting interest in understanding business finance such as cash movement and financial forecasts, I was able to steer clear of these problems.

This information completely changed the way I operated my business, allowing me to improve my decision-making ability and maintain adequate control over finances.

3. Not Setting Money Aside for Taxes Can Lead to Costly Surprises

As an entrepreneur in the journey, there is a lot to be learned in terms of experience and skills acquisition but there are some that are not really avoidable.

One such lesson I seem to have missed during my start was ensuring that I put aside a specific amount of my earnings to cover the taxes, alongside other sources of expenditure.

I was caught completely off guard when I discovered how much of my earnings would be dispensed as tax because I hadn’t planned for it around that time of the year.

This resulted in dire cash flow issues, as I hadn’t managed to save a considerable amount up to that point.

And therefore from that time onwards, I have developed a routine of saving a certain percentage of my productivity for taxes.

This prevents me from getting any shocks, allows for stable cash flow through me, and ensures that my situation is fine before the moment of tax arrives.

4. Taking on Too Much Debt Too Soon Can Cripple Your Business

Too much debt too early to bear was a mistake that nearly brought my business to its knees and set me back more than I could ever imagine.

Initially, I had thought that borrowing money was going to help me expand my business within a short period of time, but I was wrong for thinking this.

I lost track of my struggle to meet basic daily requirements, which in turn adversely affected my cash flow situation.

This mistake taught me how to expand my business gradually, and only borrow funds when it is absolutely necessary.

Do You Know? 42% of businesses fail due to a lack of demand for their product or service.

5. Failing to Build an Emergency Fund Can Sink Your Business

Another financial mistake to avoid is not having an emergency fund, and I have experienced this personally.

Because I did not have any emergency funds, I was unable to meet the urgent expenses that arose and underwent unnecessary pressure.

This has taught me to always put some cash aside for safety so that my business is not surprised at any time.

6. Neglecting Financial Forecasting Can Limit Your Growth

Another financial mistake I made, which in the long run did some damage to my business, was failing to have some financial forecast.

If that hadn’t been the case, I would have been able to manage my cash flow or expenses, thanks to which my growth was not optimal.

But as I always look for learning from mistakes, I begin any further investment only after I have a concrete plan in place so I do not experience any hiccups on my way to success in the business.

7. Avoiding Professional Financial Help Can Cost You in the Long Run

I myself don’t know how I fell into this delusion that I was able to do everything on my own and there is no need to seek professional assistance for financial matters.

This resulted in very expensive mistakes with outsourcing taxes, budgeting, and even with the investment.

At present, as I’m always in meetings with experts, they help me with decision-making related to my finances so as to save me costs and also make the growth of my business more effective in the long term.