Any investment you make, barring traditional assets like stocks, bonds, etc., is an alternative investment.

Updated Mar 9, 2026

Beyond Stocks – A Small Business Owner’s Guide to Alternative Investments

All world markets tanked due to the COVID-19 strike. Some brave ones went into the market, but most of us were scared for life, forget investing. As the markets recovered in a straight line, many people got drawn to the idea of investing. Alas, the boom bus had already left.

Since then, the market has been moving sideways, and people have gotten bored. They are searching for alternatives to park their capital, which has been at the same value in their stock portfolio for 6 years. On top of it, inflation is eating into it. Capgemini data says that 94% of investors have alternatives in their portfolio.

In this guide, I’ll educate you on these alternative investments, their various types, and why they should be a part of your portfolio in these trying times.

KEY TAKEAWAYS

- Alternative investments are investable assets that fall outside of the purview of traditional assets.

- It includes real estate, angel investments, P2P lending, crypto, etc.

- They are a great way to hedge against traditional markets.

- Only invest surplus capital, keep portfolio diversified, and follow relevant tax rules.

What Are Alternative Investments?

Any investable asset that falls outside of the traditional investables, like stocks, bonds, and gold, can be called an alternative investment.

They range from bricks and mortar to fine wine, and they tend to behave differently from public markets, which is precisely their appeal. When the FTSE 100 drops, your property or private equity holding doesn’t necessarily follow. That kind of diversification can be a powerful tool for long-term wealth building and a crucial part of portfolio diversification.

Property and Real Estate

The most popular alternative investment around the UK and even the entire world is real estate. Residential buy-to-let, commercial property, and REITs (Real Estate Investment Trusts) all offer a legitimate and reliable way to create both an income stream and capital growth over time.

Buy-to-let is a good option if you want to live like a landlord. However, it is worth noting that recent changes to mortgage interest tax relief have made it less lucrative than it once was.

Private Equity/Angel Investing

Startups are in a forever lookout for investors who have money to put in their business. Become an angel to them and exit as you make significant returns. It’s risky as many startups fail, but you can make up for the losses if just one succeeds.

In the UK, schemes like the Enterprise Investment Scheme (EIS) and Seed Enterprise Investment Scheme (SEIS) make this particularly attractive for higher-rate taxpayers, offering generous income tax relief and Capital Gains Tax exemptions on qualifying investments.

P2P Lending

An intermediary used to take his cut in traditional loans, but now there is peer-to-peer lending. Earn interest by directly lending to individuals/businesses. Returns can be attractive compared to traditional savings accounts, though the risk of borrower default is real and these investments are not protected by the Financial Services Compensation Scheme (FSCS) in most cases.

Corporate bonds are essentially loans you make to companies. They sit somewhere between P2P and stock market investing. While they offer fixed income, they also come with credit risk depending on the issuer’s financial health.

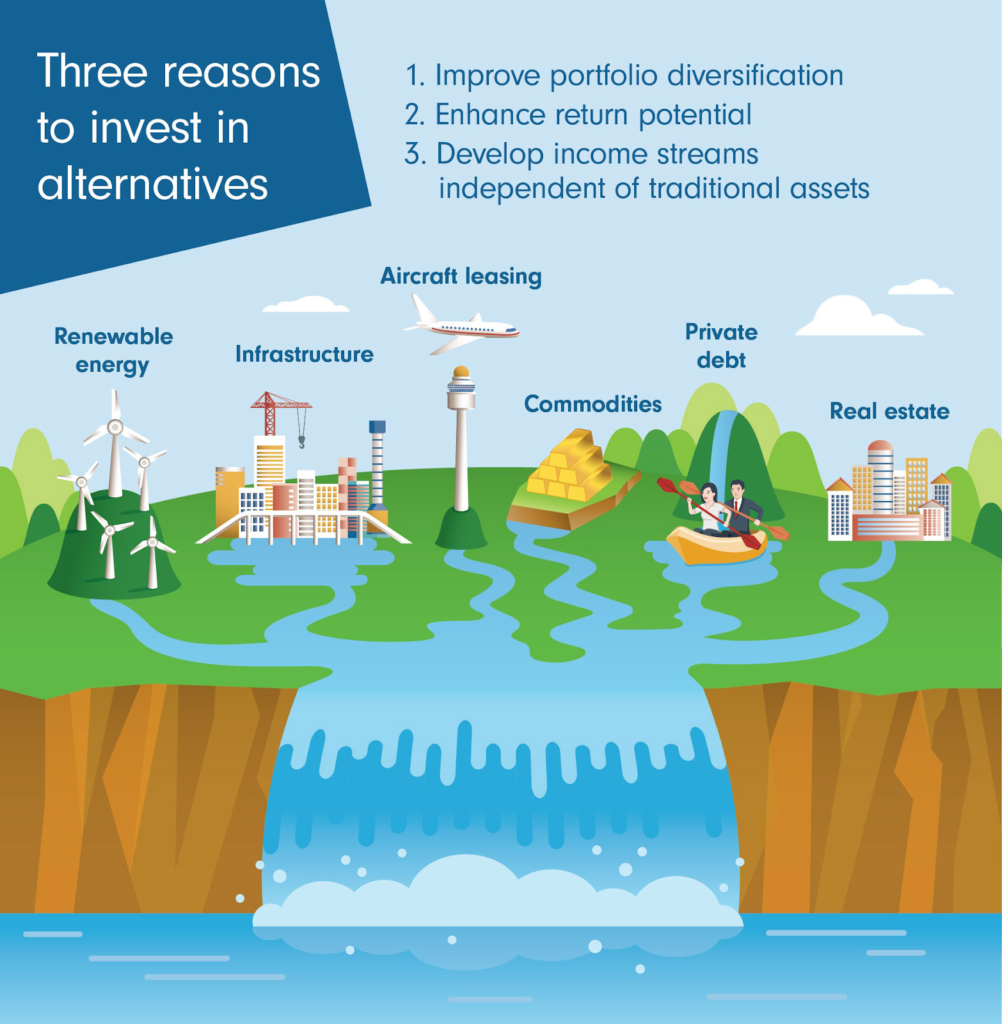

The following infographic lists three strong reasons to do P2P lending and invest in other alternatives:

Crypto

It was just a few years ago that cryptocurrencies were shunned as fringe and destined to fail. But times have changed, now they are part of the portfolio, even of the biggest of institutions.

Bitcoin and Ethereum are among the most recognisable ones, but plenty of others are present as well.

While crypto investing has come a long way in the last decade, it is still worth noting that volatility in the crypto market is unlike any other asset. Double-digit percentage swings in a single day are not uncommon. If you are a small business owner considering investing in crypto, it is a good idea to learn all you can about them. Sites like CCN are usually a good start, offering a comprehensive education on all things crypto.

Managing Risk Across Your Portfolio

Be it traditional or alternative investing, the rule of investing remains the same: invest only the capital that you won’t mind losing. Investing can be a high-risk activity and you can easily end up losing your starting capital. Fortunately, there are several strategies that can help mitigate that risk.

A diversified portfolio is one of the best approaches you can take. As the saying goes, don’t put all your eggs in one basket. It can be tempting to invest heavily into one potentially lucrative option, but there are no guarantees that it will actually pan out. That is why spreading your capital across different asset classes is the most sensible strategy.

The tax situation is another point of concern. Alternatives are generally new investment areas, so the tax situation is mostly unfamiliar. If you’re unsure how your investment activity affects your overall financial picture, it’s worth speaking with an accountant who understands both business and personal finance.

Conclusion

Stocks and mutual funds still make the majority of the portfolio pie, but alternatives are also visible now and growing fast.

For small business owners with capital to spare, alternatives offer real opportunities to not just increase wealth but also diversify income streams, which can be a crucial advantage in these uncertain times.

Author - Shourya Kumar

Finance Writer

Related Posts