The Buy Now, Pay Later (BNPL) is a financial option model, wherein users can buy an item with a low upfront payment and then pay the remaining amount in installments later on, after a set period of time.

Updated Mar 30, 2026

Why Businesses Must Use The “Buy Now Pay Later” Model With Caution

Recently, the Buy Now Pay Later (BNPL) model has soared in popularity, opening up new lifestyle possibilities that were once inaccessible to many users. Due to this, many brands have integrated the provision into their business flows.

Furthermore, customers get instant financing for the things they want without the hassle of applying for a bank loan. With only a nominal amount to pay at purchase and an installment (interest-free) system, it has become an easy way to buy large-value items with ease.

But in the rush of adoption, caution must also reign supreme. BPNL models, while mostly beneficial for business, also have their pitfalls. Let’s understand these.

Key Takeaways

- The BNPL payment method allows users to make a lower upfront payment and pay the remaining amount in installments after a set period of time

- This method attracts many risky issues, like debt and scams.

- A firm may be held responsible for such issues if stricter guidelines and implementation aren’t set earlier

- Impulsive decisions cause many users to return the items they once bought, making transactions difficult for businesses to track

Of Debt, Scams, and Other Risks of Financial Trends

New and emerging payment processing trends in the finance sector have always been double-edged swords.

They offer promising savings and increased purchasing power, but at the other end, it may also lead to an increase in scams that undo all the benefits.

For instance, news reports note that flawed BNPL plans have led to rampant scams in Southeast Asian countries, such as Thailand and Vietnam. It has triggered a murky area of peer-to-peer loans. The prospect of cash-outs is enticing, but the long-term result is indebtedness.

In response, more countries are now working on stricter codes of conduct for these payment modes. Businesses may need to place limits on outstanding payments and issue clear disclosures on the impact of these plans.

Responsible businesses do not offer a payment option for customers and wash their hands of the repercussions of their actions. Instead, they need specialized payment processing solutions that consider these possibilities and build guidelines against them.

For example, businesses can prioritize credit risk, i.e., the likelihood that a customer will be unable to repay the loan. An experienced financial services team can partner with firms to identify customer characteristics that can indicate a high level of credit risk.

AI has improved the identification and detection of fraud risk. Analytical tools can now monitor suspicious actions, such as unusual buying patterns or multiple shipping addresses, with high precision.

The challenge here is that AI is also a grey area: many scammers use related technologies for impersonation and deception.

A Thomson Reuters feature highlights that AI can help fraudsters orchestrate highly convincing scams through synthetic identities. The possibility of all-green fraud, which happens in authenticated sessions, is also increasing.

Thus, while implementing BNPL with safety, businesses need a thorough and competent risk identification and management system.

Did You Know?

While popular for fashion and electronics, BNPL is increasingly used for essential services, such as car repairs or healthcare expenses

Impulse and Sustainability Don’t Get Along

A major downfall of the BNPL model is its promotion of instant buying tendencies. When interested customers see the option, their sticker shock reduces or even dissipates for a few moments.

They may purchase a product impulsively, causing the analysis metrics tracked by businesses to spike.

However, many of these orders also end up getting returned. As it turns out, the increase you saw in your customer base was not sustainable.

A 2024 study in Computers in Human Behavior found that impulsive behavior in shopping is often linked to low self-control. No surprises there. It also noted that feeling positively disposed towards targeted advertisements made consumers more susceptible to these impulsive decisions.

It is anybody’s guess how a cheerful BNPL-focused shopping ad affects customers or prospects who are prone to impulsive behavior.

Excessive returns are not only bad for the revenue of a business, but it also paints a poor picture of corporate responsibility.

The emotion is that if a business really paid attention and cared, it would not let customer satisfaction sink so low that products needed to be returned.

Merchant Fee Spike May Be Untenable

If your business allows a BNPL payment model, the merchant would charge higher fees, as it becomes a security net for the merchant.

The Foundation for Economic Education notes that these models can incur more than double the merchant fees for standard credit cards. It could go up to 6% or more, with a flat fee in addition.

This makes it likely that future legislation may try to limit merchant fees, which may cause significant upheaval in this sector.

Volatility, and not the good kind, does not bring good tidings for either the business or its customer base.

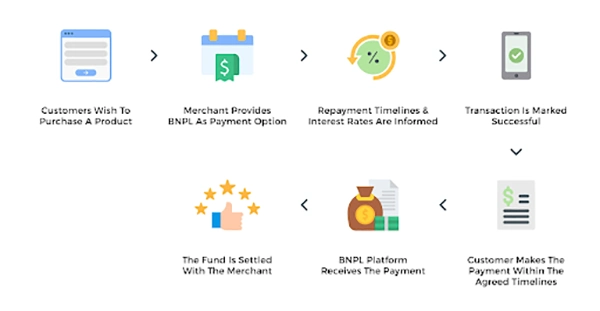

This whole process, the involvement of a merchant, can be better understood through this infographic:

Final Word

Buy Now Pay Later is the next frontier in marketing: enabling customers to find and own what their heart fancies without being restricted by expenditure.

However, from both an accounting and long-term business perspective, BNPL demands close and careful attention.

Staying alert during implementation, monitoring, and tracking of the impact on your business are both essential for safe and sustainable operations.

Author - Shourya Kumar

Finance Writer

Related Posts