Borrower’s poor credit history, high debt-to-income ratios, economic downturns, and no collateral.

Updated Mar 16, 2026

Why Faster Loan Approvals Don’t Have to Increase Credit Risk

In the traditional sense, faster loan approvals lead to higher default risk. On the other hand, stricter approval standards will lengthen the approval process.

Till the loan was approved, the risk profile of the borrower and the market situation used to change drastically. But with no other option available, lenders had to go ahead with a decision that was based on months-old data.

But that’s not the case today. AI automation has accelerated to process to an extent that you don’t have to choose between approval speed and credit risk.

Firms are performing risk assessments fast with 360-degree AI tools and approving the loans even faster. AI integration in loan approvals has not only sped up the process from weeks to minutes, but also enabled risk prediction with 90% accuracy.

Modern loan origination software eliminates the gap between data and decision.

In this article, I’ll explain all about why automation is trumping the manual in the lending business. The following sections list out decisions to move onto the AI bus to quicken the loan approvals while maintaining a decent credit risk.

KEY TAKEAWAYS

- AI automation has quickened the loan approvals.

- Many people believe that it is being achieved by increasing credit exposure, but that’s not the case.

- Credit risk is also better managed with AI, along with resolving other manual underwriting drawbacks.

- You no longer need to choose between a quicker loan approval process and maintaining a decent risk exposure.

The Hidden Risk of Human Judgment

Will two humans, given the same work, do it the same? No right. Then why do we assume that two underwriters assessing the same borrower profile will reach the same conclusions?

It will be different depending on which financial ratios they weighted most heavily, which qualitative factors they found most persuasive, and how much time they had. Inconsistent risk assessments emerge as different underwriters emphasize different factors, and without a standardized workflow, each analyst may assess a borrower differently, creating friction across teams.

That variance accumulates into portfolio risk over time. Not through a single bad decision, but through the aggregate inconsistency of hundreds of decisions made by different people interpreting the same policy differently.

A lender running manual origination across 400 commercial loans is not applying a consistent credit standard. They are applying the collective judgment of however many underwriters reviewed those files.

Loan origination software does not remove judgment from lending. It removes the variance that undermines portfolio quality at scale, enforcing the same eligibility criteria, financial ratio thresholds, and risk tier definitions on every application.

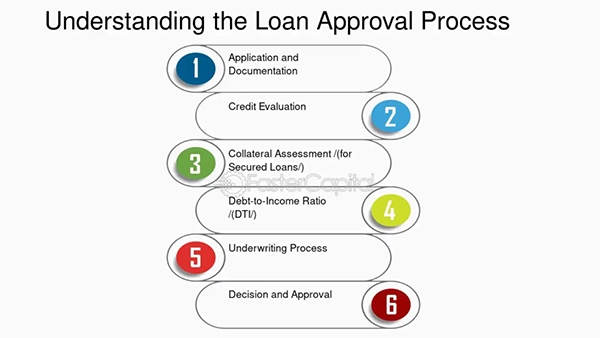

A regular loan approval process, which these software have accelerated by a huge margin, looks like this:

The Adverse Selection Problem Nobody Talks About

Manual, slow approvals screen better and improve the credit risk of the lender, right? Wrong. It’s actually the opposite. Good credit borrowers simply let go of a lender with a sluggish approval process.

Manual processes lose 20 to 30% of applicants to abandonment before a decision is reached. The borrowers most likely to abandon a slow process are the ones with options: low-risk, financially strong businesses that have access to multiple lenders.

The borrowers most likely to wait through a 30-day manual review are the ones who have already been declined elsewhere or who have no alternative.

A slow origination process does not signal diligence to the market. It signals to the best-quality borrowers that there is a faster lender worth approaching instead. Lenders who believe slow approvals protect credit quality may be selecting for exactly the borrower profiles they were trying to avoid.

Lenders lose 2 loans for every 1 closed, according to Cornerstone Advisors. Over half of financial institutions abandon >75% of loan applications due to friction. Speed under 5 minutes cuts abandonment to 25%, doubling closed deals without lax underwriting

Why LOS Outsmarts Manual Teams

Manual underwriting is a step-by-step process, with each step being dependent on the previous one.

That sequence creates two problems simultaneously: delay between steps, and variance in how each person interprets what they receive.

Loan origination software breaks both constraints at once. Document verification, financial ratio analysis, policy rule application, and concentration limit checks run in parallel rather than in series. The approval timeline compresses not because any step was removed but because no step waits on another.

The more significant intelligence gain is at the policy layer. When credit rules are configured in the system rather than carried in underwriter heads, policy applies identically to every application regardless of who reviewed it, how busy they were, or which factors they found most compelling.

This consistency produces a data asset that manual origination cannot generate: a clean, comparable record of every decision, the conditions that triggered it, and the outcomes that followed.

Delinquency patterns in specific asset categories or loan structures surface in the origination data before they accumulate into loss events. Thresholds that are producing unexpected stress adjust quickly because the signal is clear, current, and traceable to the specific policy conditions that created it. Risk management stops being a periodic review of what went wrong and becomes a continuous calibration of what the data is showing right now.

Speed and Rigor Are the Same Variable

Traditional manual lenders might be thinking that the new automated lenders are making a grave mistake by approving loans in a fraction of the time it takes manually. They would think that it would only increase the risk exposure of those lenders.

But they are so wrong.

The modern lenders are running a more disciplined process on fresher data. When credit policy lives in a loan origination system rather than in underwriter interpretation, it applies uniformly at the speed at which the system processes information. When data is ingested at the application rather than gathered manually over 30 days, the decision reflects the borrower’s current condition rather than a financial profile that has already aged.

The speed-versus-risk trade-off is not a fundamental tension in lending. It is a symptom of manual processes that cannot be both fast and consistent simultaneously. Automated origination resolves that constraint by making consistency the mechanism of speed, and data freshness the foundation of credit quality.

Now you know why loan approval speed is no longer related to the credit risk. In fact, manual underwriting had many other drawbacks that the loan origination softwares are resolving.

Here’s to your faster approvals and lower risk!

Author - Shourya Kumar

Finance Writer

Related Posts