Box 12 is a report of particular kinds of compensation and benefits with a letter code. These can be retirement savings, health cover expenses, deferred compensation, or some tax payable.

Updated Mar 9, 2026

W2 Box 12 Codes List: Meanings, Tax Impact & Filing Guide

Have you ever looked at your Form W-2 and seen that Box 12 had letters such as D, DD, W, or AA, then you may have been confused as to what they represent. Unlike other boxes, which indicate the amount of salaries and taxes, Box 12 reports the type of compensation, benefits, and tax-related adjustments using letter codes. While your employer’s internal payroll services handle these calculations throughout the year, understanding them is crucial for your personal records.

The following W2 Box 12 codes will give the IRS much information related to the retirement contribution, health benefits, and other taxes that could be outstanding. We have explained everything about W2 box 12 tax codes in this blog, so let’s get into it!

Key Takeaways:

- Box 12 reflects special compensation items with the help of letter codes (A-II).

- Conventional retirement investments (such as Code D) decrease taxable income.

- Roth contributions AA, BB, EE do not decrease current tax rates and payments.

- Code DD is informational, and it does not raise your current tax bills.

The Box 12 codes should be treated with care to ensure that they are entered as they appear so as to prevent filing errors.

What is W2 Box 12 Codes?

Form W2 box 12 codes are an important reporting area and reflect certain kinds of compensation and tax adjustments that are represented using regular wage boxes. Although the amount of your total taxable wages is in Box 1, Box 12 breaks down further and provides more details as to how the total taxable wages were computed. This level of detail is similar to how a business manages its accounts payable services to ensure every expense is categorized correctly.

Each type of entry is denoted by a letter code, in which the employers use A to II. Since employees can be enrolled in more than one benefit plan, eg., retirement plan, health savings account, or deferred compensation plan, box 12 can have more than one line. Many companies utilize professional bookkeeping services to track these various employee benefits accurately before they ever reach the W-2 form.

The amounts listed here may:

- Reduce your taxable income.

- Get incorporated in Box 1 salaries.

- Activate further reporting on other forms of tax.

Box 12, in other words, provides the IRS with a closer examination of the elements of your compensation package.

Importance of Box 12 Form W-2 in Tax Filing

Most taxpayers think Box 12 is not much, but it has a great portion in the final tax result. The information in this box has a direct impact on the number of forms that should be filled out and the amount of income that is taxable. For those who manage their own business, ensuring these figures are correct is a vital part of management accounts services and internal financial oversight.

For example:

- The contribution made in retirement can reduce your taxable wages.

- HSA contributions have to be reported separately.

- Some deferred compensation plans could attract incremental taxes.

- The informational codes are used in order to adhere to the healthcare and benefit reporting requirements.

Mistakes in filling in Box 12 codes may result in penalties, underpayment, not receiving deductions, or receiving delayed refunds. This is why many individuals and corporations prefer tax outsourcing to ensure that complex codes are handled by experts. The knowledge of these codes will help make sure that your Form 1040 is reflective of the true income and that the taxes are treated correctly.

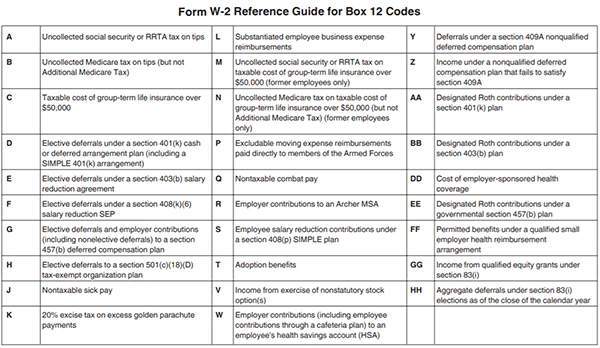

W2 Box 12 Codes Explained: Complete List & What Each Code Means

In box 12, there are more than 25 possible letter codes, each of which indicates a particular type of finances. Below is a simplified yet detailed breakdown to help you understand what each group of codes represents and their effect on your tax return. Also, to understand these terms in full, you can take help from tax return services to avoid any mistakes.

Social Security and Medicare Codes

Certain code 12s are associated with taxes that were not entirely collected via withholding of payroll. For businesses, tracking these uncollected amounts is as critical as managing their accounts receivable services outsourcing to maintain cash. Let’s check them here:

| Code A: Social security tips tax that is not collected is reflected here. In case your employer was not able to take out as much as he should have paid you in terms of tax, he is liable to do the rest at the time of filing. |

| Code B: Uncollected Medicare application tax on tips. This amount, like Code A, should be reported on Schedule 2 of Form 1040. |

| Code M: Uncollected social security tax on life insurance for group-term purposes of more than 50,000 (only to former employees). |

| Code N: Uncollected Medicare tax on group-term life insurance (former employees). |

Retirement Contribution Codes

The most common items that are reported in Box 12 are retirement plan contributions. These are often reconciled during year end accounts ct returns services to ensure that employee deferrals match company records.

| Code D: Conventional 401(k) contributions. These decrease your taxable wages in Box 1 and may entitle you to the Saver’s credit. |

| Code E: The 403(b) type of contributions is most often used by nonprofit workers and those in public schools. |

| Code F: SEP retirement investment amount is noted here. |

| Code H: Plans of tax-exempt organization 501(c)(18)(D). |

| Code S: Denotes simple IRA contributions. Such codes generally result in a decrease in federal taxable income, but they are also included in the wages to Social Security and Medicare. |

| Code AA: Roth 401(k) contributions. |

| Code BB: Roth 403(b) contributions. |

| Code EE: Roth government 457(b) contributions. Unlike traditional contributions does not decrease current taxable income but may be withdrawn in retirement tax-free, provided the requirements are met. |

Healthcare Insurance Reporting Codes

Federal reporting requirements have made reporting associated with healthcare more frequent in Box 12.

| Code DD: Employer-sponsored health coverage cost. This is a mere figure that cannot add to your taxable income. |

| Code W: Contributions of the employer and the employee to a Health Savings Account (HSA). These sums should be carried in Form 8889 and may have an impact on your deduction limits with HSA. |

| Code FF: The benefits of a qualified Small Employer Health Reimbursement Arrangement (QSEHRA). |

Code of Compensation and Special Income

There are Box 12 codes that show taxable compensation that might have been reported in your wages. If you are unsure how these impact your filing, consulting with specialized accounting services can provide clarity on how special income is taxed.

| Code C: The taxable value of group term life insurance in excess of 50,000. This is already factored in Box 1 wages. |

| Code V: Enterprise of non-statutory stock options. Taxable wages also include them. |

| Code Y: Deferrals of 409A nonqualified deferred compensation plans. |

| Code Z: The income under deferred compensation that breaches the IRS 409A regulations. This could be paid a penalty tax of 20 percent. |

Military Code and Special Benefit Codes

Some box 12 codes are only applicable to military members or special benefits programs.

| Code P: Reimbursements of excludable moving expenses of active-duty Armed Forces members. |

| Code Q: Nontaxable combat pay. |

| Code T: This shows adoption benefits. The excludable portion is determined by the use of Form 8839. |

Other Less Common Box 12 Codes

| Code J: Informational Nontaxable sick pay. |

| Code K: Excessive parachute payments of golden parachutes will be subject to an excise tax of 20%. |

| Code L: Reimbursements on employee business expenses that are substantiated. |

| Code R: Contributions by the employer to Archer MSA. |

| Code GG: Qualified equity is a source of income. |

| Code HH: Section 83(i) deferrals that are aggregated. |

| Code II: The payments of the Medicaid waiver are not included in gross income. |

W2 Box 12 Codes Impact on Taxable Income

Not every code impacts the taxable income directly. However, it is important to know how to classify them correctly. Just as a business must carefully handle vat return services to stay compliant with local laws, an individual must classify Box 12 codes to avoid IRS audits.

- Tax-cutting codes that generally make income taxable: D (401(k)), E (403(b)), F (SEP), G (457 traditional), H, S.

- Codes which do not decrease taxable income: AA, BB, EE (Roth contributions), DD (Health coverage cost), FF.

- Box 1 Wages Codes Already Included: C, V, Z.

- Codes Subject to Extra Tax: A, B, K, Z.

It is always necessary to ensure whether the amount has already been included in your taxable wages before making any adjustments.

W 2 Box 12 Codes: Misconceptions

One of the most frequent mistakes concerning the filing is a misinterpretation of Box 12 codes. Most of the taxpayers assume that all entries are additional income, but most of the codes in box 12 W2 are informational or fall within box 1.

An additional stereotype is that Code DD raises taxes, which in reality it does not. Also, others feel that Roth contributions lower taxable salaries. They are not made to lower the taxable income, but are put after paying taxes.

Final Words

W2 Box 12 codes are not as confusing as it might seem because they give detailed information on the contributions to retirement, your healthcare benefits, deferred compensation, and some tax adjustments. Note that not all codes raise your taxable income; some of them actually work to lower it, and some are used only for informational purposes.

Author - Dushyant K

Finance Writer

Related Posts