The Top 5 Common Credit Report Errors and How to Fix Them

Did you know? According to the Federal Trade Commission (FTC), one in five people will have a credit error on their credit report.

Credit cards are the most used asset in today’s fast-paced cosmos of the metro cities.

Many people rely on this tool for managing their lifestyle or buying desired things in installments.

However, a bunch of people face many errors and problems that ruin their experience of shopping and sometimes make them prone to fraud and scams.

Mostly, the audience doesn’t know how to win a credit dispute, so it’s better to understand some prevention strategies and safeguard themselves from compliance

Being an internet geek and a credit card user for the last 7 years, I will share some valuable insights on this concept with the readers.

Let’s get started!

Key Takeaways

Have you noticed? Sometimes you enter the correct credentials, and still it says invalid. Find ways to deal with it

Don’t get fooled by duplicate accounts; make sure to never reveal your banking identities.

Outdated and Inaccurate info can depreciate your credit scores; make sure to assess it regularly.

Frauds and identity scams are most prevalent nowadays; stay ahead of them.

Never be entertained by missed payment notifications of accounts that are cleared

1. Incorrect Personal Information

To start this segment, we have the most frequent issue that occurs among the users, and that is incorrect personal information. It mostly happens because of misspelling or misnumbering of your correct code.

Although incorrect personal data in credit reports appears to be minor, it creates confusion among lenders and creditors who depend on accurate information for their decisions. Your credit report could contain information from another person who shares similar name and location details, making the information inaccurate.

Interesting Facts In a study, the FTC found that 5% of U.S. consumers have an error on their credit report that “could lead to them paying more for products such as auto loans and insurance(FTC),

2. Duplicate Accounts

Next off, I have a problem that is mostly caused by software glitches and errors and it’s the availability of duplicate accounts. Having multiple incorrect listings for the same account on your credit report can lower your score and make it seem like you have more debt than you do. Sometimes, lenders can accidentally create duplicate entries when they report data due to simple mistakes, and errors can also occur during data processing.

3. Outdated or Inaccurate Account Information

As per my experience, your credit report may include outdated or incorrect account activity. Mistakes in your credit score often arise from accounts that remain open when they should be closed or erroneous late payment designations that shouldn’t impact your credit rating.

Your trustworthiness can significantly decline if a debt or loan is marked as outstanding after you’ve paid it in full.

It’s crucial to promptly address inaccuracies in your account status, as they can severely affect your credit.

Reviewing your credit report accounts to verify their correct status is an essential step to resolving this problem.

Any outdated or inaccurate information requires you to dispute it through the credit reporting agency.

The bureau will verify the information with the creditor until the incorrect details are confirmed and subsequently updated or removed from your report.

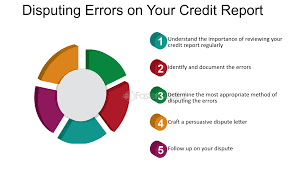

Intriguing Insights This infographic shows the various disputing errors on credit cards

4. Unfamiliar Accounts or Fraudulent Activity

Imagine waking up one day and being notified by an unknown payment trigger that credits have been deducted. It sounds like a nightmare, doesn’t it?. Many people go through this situation every while, and they don’t know how to tackle this, and they rush in with so many mistakes. Well, don’t worry, I’ve got you covered. Just follow the action plan I’m giving below:

Must respond rapidly when you see any fraudulent activity.

Immediately inform any authorized federal body

Enable alert alarms in your banking apps

Regular credit monitoring helps you discover unauthorized activity at its initial stages

5. Missed or Late Payments That Were Paid on Time

The amount of transaction tendency drastically impacts your credit score, and submitting your EMIs late can harm your financial integrity and lead to many unforeseen consequences. In the future, there are possibilities of loan rejections if you are listed with late payments multiple times.

To prevent this I suggest that always asses your paid bills on time and check-up on instalments that are cleared but remains unpaid. Talk with officials and solve this concern as soon as possible. After verifying the timely payment, the provider must communicate with the credit bureau, which will update your current account report.

Conclusion

To sum up this entire segment, I just want to say that Many individuals fail to realize how often errors can appear on credit reports, and these inaccuracies can significantly impact their financial situations.

It’s crucial to regularly review your credit report, as this process allows you to spot errors such as incorrect personal details, repeated accounts, outdated information, missed payments, and fraud activity.