A certificate of insurance is an important document that proves that you have active insurance. It contains the policy details such as the insured person or business’s name, policy number, date of expiry, and more.

Updated Nov 26, 2025

Certificate of Insurance: Who Needs it and How to Obtain One?

If there’s one document businesses cannot afford to lose, it is the certificate of insurance. This important document serves as proof that your business is shielded against risks and liabilities.

When you’re starting out, the COI allows vendors, contractors, and clients to have trust in you and shows that you’re serious about the company and will take full responsibility.

We have covered everything about the certificate of insurance and the certificate of liability insurance in this blog. So read till the end and take notes!

What is a Certificate of Insurance?

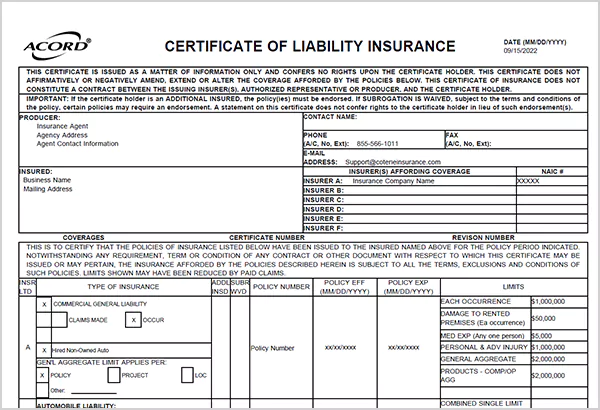

A certificate of insurance is a legal document issued by the insurance provider in the name of the policyholder. It contains all the major details regarding the policy, like its coverage, policy limits, dates of effectiveness, and more.

The entire insurance policy is tough to read, as it’s full of technical jargon that can not be grasped easily by common people. As all the business dealings and transactions are based on the insurance policy, a COI, which is basically a one-page document, simplifies everything and becomes a significant part of financial planning and core accounting services.

Notably, the COIs in the US follow a standard format known as ACORD 25, which is recognized by all industries and can be easily reviewed.

We have introduced you to what is a COI; now, let’s go ahead and understand more about this document in detail.

Why is the Certificate of Insurance Form Important?

A certificate of insurance is more than just a formal document; it is a factor of trust and transparency. A client or business wants to work with companies with COI because of the financial support it provides against unexpected losses and damages that often occur in the course of the project.

Here are more reasons why this form holds such significance:

- Proof of Coverage: Having a written note of what is insured and covered helps to get an idea and plan the action plan accordingly. It also gives confidence to the client that you will be able to manage the losses if something bad happens.

- Legal Requirement: The government does not pass any tender for any project if the certificate of insurance is missing. Even the normal business contracts and lease agreements are fulfilled with COI.

- Risk Management for All Parties: The COI mentions coverage scope clearly, helping businesses coordinate with bookkeeping services to manage financial clarity.

- Acts as a Verification Tool: Having a COI makes the company trustworthy in the eyes of the vendors and investors. Instead of sending full policy details, one can share the certificate of insurance, which summarizes the policy information and rules of general compliance.

- Helps to Settle Claims: A COI shows that you were insured during the particular period of damage or loss, and now it is the duty of the insurance provider to settle down claim. It eliminates the misunderstanding regarding the coverages and facilitates in smoother settlement process.

Also Read

Who Needs Certificates of Insurance?

COI is not just for large-scale companies, but for every person or business engaging in financial and legal activities will require a certificate of insurance. It serves as evidence of coverage whether it is a business transaction, a service agreement, or a project with a third party involved.

We have classified who needs to have a COI below:

- Companies Making Financial Transactions: Every company or person who makes a business deal that involves procuring investments and investing in assets should have a COI. This includes: retailers, wholesalers, and suppliers.

- Small and Medium-Sized Businesses: To build trust; they commonly simplify workflows using payroll services and accounts payable services

- On-Site Projects: Contractors, builders, and service providers also maintain internal review reports using management accounts services for accurate tracking. So, it is important to have a COI to make a claim instantly when needed and to gain the trust of all the parties involved in the project. This includes: real estate builders, contractors, and online sellers.

Also Read

What Information Does Certification of Insurance Contain?

Even though the certificate of insurance is a one-page document, it contains all the key details and aspects of your policy. These details ensure that your business is safe against all the potential risks. Let’s take a look at these details:

- Insured Person/Business Information: The document includes contact information of the individual or the company that owns the insurance policy, including contact details and address.

- Insurance Company Details: COI includes the name of the insurance provider with their legitimate authorization number, making sure the company is verified and claims are cleared under government supervision.

- Type of Coverage: Whether you choose professional liability, commercial auto insurance, workers’ compensation, or general liability insurance, it is clearly mentioned in the COI.

- Policy Number: Every insurance plan and policy holds a unique number, which confirms that the coverage is working and can be traced directly to the insurer.

- Coverage Limit: often relevant for credit control and accounts receivable services outsourcing Limits. Like per occurrence limit, aggregate limit, property damage limit, or personal injury limit establish the expectations for the policyholder and for the clients.

- Signature of Representatives: Government-authorized stamp and signature of the representative of the company and policyholder are marked at the bottom of the document.

How to Obtain Insurance Certifications?

A certificate of insurance must be handy for every businessperson who wants to demonstrate professionalism and ensure their business is protected with coverage. This document gives contractors, freelancers, and investors to have faith and invest in your business.

Here’s how to get your COI:

- Step 1: Contact the Insurance Company or Broker: The first thing to do is get in touch with the insurance broker. They are the right holders to issue your COI with all the information that reflects your present issuance cover. Most providers accept online requests and send the COI via email.

- Step 2: Offer Correct Info of Certificate Holder: You must provide correct information about the certificate holders, like name, company, and email address.

- Step 3: Mention Your Requirements: Your client may need certain information or assurances on the COI, like the total coverage amount, waiver, additional insured, and more. You need to mention all these additional requirements to the provider so that they can incorporate the right endorsements and wording.

- Step 4: Receive the Certificate and Store It Securely: Your insurance providers will email the certificate within 24–48 hours of the discussion. After receiving the file, download it and save it in your digital folders of documents.

That’s it, every time you want a COI, these are the simple steps you need to follow. Just make sure to update your COI regularly so that you continue to stay out of risk with the policy coverage.

Common Mistakes to Avoid

Many businesses fail to obtain a COI because they knowingly or unknowingly fail to comply with or provide the right details. These are the common mistakes that you must particularly take care of while obtaining a certificate of insurance:

- Failing to Check Certification Details: Most companies will believe what is on the COIs without verifying the information. You must always check the policy number, the type of cover, limits, and expiration date. Ensure that the information is similar to your pact or contract. Any slight difference is enough to cause issues in the course of a claim.

- Failing to Renew Outdated Certificates: A COI can only be valid provided the underlying insurance policy is active. When a policy expires or is renewed, the previous certificate is invalidated. Monitoring of the expiry dates and demanding a new COI is important for continual protection.

- Omitting Certificate Holder’s Name: It is essential to provide a proper name and address of the certificate holder, the one who requires evidence on insurance. This section may make mistakes because of the confusion or rejection that may occur during audits, verification of the client, or contract signing.

- Failing to Keep the Copies of Issued Certificates: It is significant to maintain a record of every COI you are giving out or receiving. You must maintain a sheet with dates and the certificate number to track the validity dates and renewals.

Wrapping Up!

Certification of insurance is a vital document for a person or business, and being proactive in managing these certifications is as significant as insurance itself. Make sure to have a safe file to keep these insurance certifications and always check the dates, policyholder’s name, and coverage allowed before accepting it.

We have covered how to obtain a COI to the common mistakes everyone must avoid in the process in this blog. Hopefully, the info will help you in obtaining and keeping track of the documents well.

Author - Veeramanchineni Lalitha

Masters of Business Administration from St Joseph's Institute of Management (Banglore)

Related Posts