How to Optimize Remote Financial Management for USA Expats

As someone who loves hopping through different countries, experiencing different cultures, sampling delicious delicacies, and meeting amazing people, I can say that the joy it brings cannot be explained in words.

But unfortunately, various challenges also come complimentary with the joys, the major one being managing the finances. It is estimated that more than 4.4 US citizens are living abroad and are required to comply with these regulations. (AAR: How Many Americans Live Abroad?)

You might be surprised to know that as a US expat, I had to pay taxes back home and meet various other obligations? Kind of unfair, isn’t it? But with the right tools and strategies, I am able to remotely manage all my finances and stay ahead of any financial obligation. Curious to know more? Keep reading as I walk you through six methods I use to optimize my finance management systems.

Choose the Right Bank Accounts

While maintaining your U.S. account has benefits like convenience, having a separate international account streamlines transactions in your new travel location, especially when purchasing things.

Many U.S. banks offer expat-specific bank accounts and services that let you access your reserves from anywhere. However, I would still advise you to select a bank account that has minimal international fees and good global ATM access.

You can consider online banks that specialize in expat services, such as those offering no foreign transaction fees or advantageous currency exchange rates. A digital-only bank may also streamline your day-to-day financial operations by providing budgeting tools and better control over international transfers.

Understand Tax Implications and Compliance Requirements

When you move to another country, the most logical thought would be, ‘I don’t have to file taxes in my home country.’ Right? Sorry to disappoint you but, unfortunately, as a U.S. expat, the government still requires you to report your worldwide income; failing to do so could lead to penalties.

One key aspect of this compliance is the Foreign Bank Account Reporting (FBAR). U.S. laws require expats to report any foreign bank accounts where the total value exceeds $10,000 at any point during the year.

To keep up with these legal requirements, you can work with a tax professional who specializes in expatriate tax issues. It might also benefit you to look through online resources such as this FBAR filing process guide that will help you understand the steps required to file your FBAR and avoid penalties.

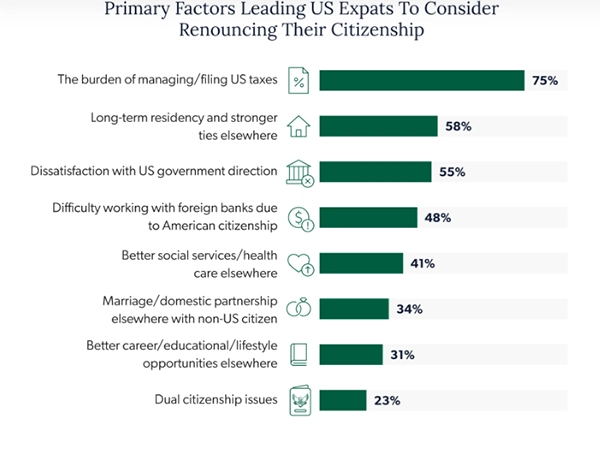

DO YOU KNOW? Various US citizens these days are considering renouncing their citizenship, the major reasons for it are as follows:

Leverage Global Money Transfer Services

If you live abroad, there are high chance that you will need to send money back home at some point. That could be to facilitate projects or maybe to a loved one. No matter the reason, we can all agree that sending money between countries can be an expensive affair.

Fortunately, we now have several pocket-friendly and fast money transfer services. A good example is PayPal, which allows you to send money securely from anywhere in the world instantly at competitive rates.

Always choose a money transfer service that prioritizes security and reliability. A good digital payment solution provider should offer real-time tracking and secure encryption to ensure both you and the recipient have end-to-end protection.

Take Advantage of Tax-Optimized Investment Accounts

Are you planning to invest your money back home while living abroad? If yes, you need to plan carefully to minimize your tax liabilities while maximizing returns.

Are you aware that expats can still contribute to tax-advantaged accounts like IRAs or 401(k)s even while abroad? That’s right, and if you plan on returning to the U.S. one day, it is vital to stay informed about the rules surrounding these accounts.

In some cases, you may be able to contribute to a U.S. retirement account if you continue to meet specific income requirements. Additionally, some expats use offshore investment accounts to take advantage of different tax structures, based on the country they’re residing in. The goal is to develop an investment strategy that compliments your long-term financial goals.

Use Financial Apps to Track Your Spending

I understand that managing your finances remotely can sometimes feel overwhelming. One way that helps me keep up with everything is by using financial tracking apps.

Tools like Mint or You Need a Budget (YNAB) allow you to sync your accounts, track spending, and set budgets all in one place. You also get to categorize your purchases and set limits, which can help you stay within your financial goals.

Additionally, these apps can also alert you to any irregular transactions or overspending, which does a good job of helping you maintain a clear picture of your financial situation.

TRIVIA There is no such thing as the typical American. The US is often called a melting pot because its people come from many different backgrounds and cultures.

Set Up Alerts for Currency Fluctuations

Living in a country that uses a different currency means you need to monitor exchange rates, especially when transferring large sums of money. Currency fluctuations can largely impact the value of your income and savings, so I would suggest you monitor these changes closely.

Fortunately, many apps and websites like XE Currency or OANDA enable you to set up alerts for specific exchange rates; this can help you make better judgements about when to convert money or send payments.

Conclusion

As we discussed in this article, having the right tools and staying informed about the various banking, money transfer, and tax requirements can help effectively simplify your finance systems and ensure you remain compliant with U.S. regulations.