Ans: It is slower initially, but it saves weeks by providing instant audit clarity.

Updated Mar 23, 2026

Why Accountants Are Focusing More on Team Communication

“Numbers are the narrative, but communication is the language that explains the plot.”

If you still picture an accountant as a solitary figure hunched over a ledger in a silent room, it is time for a reality check. In 2026, the profession experienced its most significant transformation through the introduction of new changes that will continue to shape its future development.

As Peter Drucker, American consultant, once said, “The most important thing in communication is hearing what isn’t said.” The finance industry faces critical threats because unspoken information often leads to monetary losses and brand damage.

Key Takeaways

- Communication is the core component of financial compliance.

- Informal off-channel chats must be integrated into official records.

- Dialogue acts as a secondary audit trail in case of complex transactions.

- Active dialogue prevents financial errors and mitigates hidden fraud risks.

Communication as a Problem with Compliance

A simple misunderstanding can later turn into a headache. When teams don’t communicate, compliance isn’t just difficult; it becomes impossible. Regulators now demand more than just the ‘what’; they want to know the ‘why’.

Seamless interactions with clients are not the only requirement, but the conversation needs to be documented and shared across the team so that everybody is on the same page.

To visualize the direct impact of communication on compliance, consider this ‘Compliance Traffic Light’ system, which shows how clear communication leads to audit success.

Informal Channels’ Ascent

Most individuals are more likely to send a quick Slack message or a WhatsApp text than a formal memo. While these tools make us faster, they also create ‘ghost data.’

When crucial financial decisions are taken through off channel communications, the official record remains blind to the context.

Fun Fact: The word accountant comes from the French word ‘Compter’, which means to count or tell a story.

It is essential to encourage teams to bring those sidebar chats back into the light of official platforms to ensure that the soul of the data isn’t lost. Reducing the gap between casual chat and formal records is the key to surviving a modern audit.

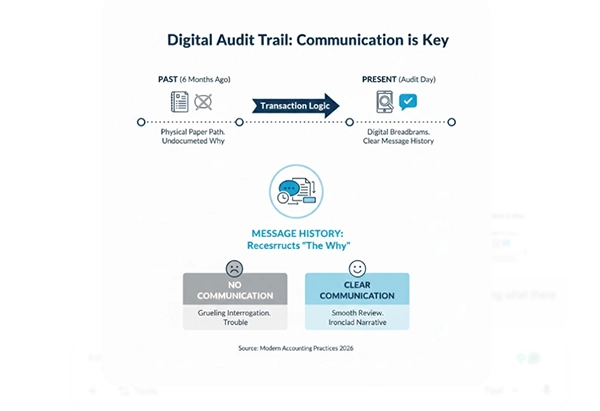

Audit Trails and Documentation

Audit trails have evolved from physical paper documentation into automated electronic records. If you can’t explain why a specific journal entry was made six months ago, you’re in great trouble.

The focus on communication is there because a message history is often the only way to reconstruct the logic behind a transaction.

It is the difference between a smooth review and an exhausting interrogation, making sure that your financial narrative remains protected under the strictest regulatory scrutiny.

The visual shows the move from unreliable paper trails to modern digital records, focusing on how a clear message history helps auditors easily track and understand transactions.

Implications for Risk Management

Risk isn’t just about the market volatility; it is about human error. Most fraud cases start when two departments fail to establish proper communication links. The inability of teams to share data results in a visibility drop, which further creates new security risks.

By tightening how vendor agreements and internal approvals are discussed, a safety net gets created. Clear dialogue acts as a deterrent to malpractice because it ensures there are always ‘multiple eyes’ on every significant decision.

Useful Actions for Accounting Teams

Now the question is, how do you turn your team into a communication powerhouse? It starts with a solid internal control framework that treats dialogue as a primary control. Here are some steps that you can take today:

- Move business discussions from personal apps to secure and logged platforms.

- Don’t just email reports; discuss the trends and issues face-to-face monthly (even virtually)

- Ensure that ‘urgent’ means the same thing to everybody on the team to avoid unnecessary panic at the last moment.

Did You Know?

Global firms were fined over $2 billion in 2025 alone, specifically for failing to archive business-related text messages.

Beyond the Spreadsheet

While technology automates the data, it is the human insight that provides the necessary content, ethics, and professional judgment to turn those figures into meaningful business strategy. We use numbers to represent value, but value is created through collaboration.

By focusing on how conversation is done, you are not just protecting your company; you are building it with a smarter financial culture.

Accountants are now not only record-keepers, but they are proactive strategic partners. They help businesses to make clear and informed financial decisions for long-term success.

Author - Dushyant K

Finance Writer

Related Posts