Ans: The open banking technology uses an API that seamlessly integrates bank accounts to accounting software or platforms, providing the features of real-time management and automation of many manual tasks.

Updated Apr 23, 2026

How Accounting Platforms Integrate Open Banking

Accounting platforms serving multiple businesses have always wanted to integrate open banking for years. It is favoured so much as it reduces reliance on manual CSV imports, automates reconciliation, and meets Making Tax Digital requirements with real-time connectivity.

But integration varies depending on how infrastructure is actually delivered. The providers optimized their pricing, onboarding processes, and more for other enterprises and fintechs, but not for SaaS platforms operating with changing deployment cycles and unit economics.

Let’s understand how this infrastructural gap is closing every day and what it means for accounting software providers.

Key Takeaways

- Earlier, the open banking infrastructure was only focused on some markets, but technological developments forced them to adapt accordingly.

- Scaling platforms now need to adapt and provide genuinely beneficial features with aligned infrastructure to actually survive in the market.

- Most growth-stage platforms earlier operated on manual processes and time-consuming strategies, as they didn’t have any other choice.

- As technology becomes inclusive, the infrastructure gap keeps shortening, forcing accounting platforms to adapt with it to remain competitive

Infrastructure built for a different market

The first wave of Open Banking infrastructure providers focused on large enterprises, banks, and global fintechs. Their business models reflected this focus: enterprise pricing tiers, extended implementation timelines, and compliance frameworks designed for high-volume operations.

For growth-stage accounting platforms, typically 10 to 200 employees serving SME clients across the UK, these enterprise-first providers didn’t align well with platform requirements.

Implementation timelines often extend over many months, far beyond the usual SaaS product development cycles. Pricing models estimated enterprise budgets and transaction volumes that didn’t quite match the unit economics of smaller platforms.

Most providers specialised in either data access (Account Information Services) or payment initiation (Payment Initiation Services), not both, forcing platforms to manage multiple vendor relationships for complete workflows.

The technical infrastructure existed. The regulatory framework was clear. But the delivery model didn’t fit the operational reality of platforms building for the SME accounting market.

What scaling platforms actually need

The infrastructure requirements for accounting platforms differ from enterprise fintech providers in several key areas.

Regulated access through authorised infrastructure. Platforms need to operate within FCA-regulated frameworks through established models such as agent arrangements, without undergoing lengthy authorisation processes and significant investment. These models provide regulated access, but were more commonly adopted by enterprise customers.

Unified data and payment capabilities. Accounting workflows require both real-time transaction data (for reconciliation and financial reporting) and payment initiation (for supplier payments and payroll). Managing separate vendors for AIS and PIS adds integration complexity and ongoing vendor management overhead.

Deployment speed aligned with SaaS cycles. Platforms work on product velocity. Infrastructure integration usually aligns more smoothly with Saas product cycles, often measured in weeks rather than quarters, to maintain release schedules.

Scalable pricing that grows with the platform. Fixed enterprise minimums and volume commitments don’t work for platforms scaling from 50 to 500 customers. Usage-based pricing that scales with actual transaction volume matches their business model.

These aren’t feature preferences. They’re operational requirements that determine whether integration is viable at all.

The market is adapting

A second wave of Open Banking infrastructure providers emerged specifically to address these gaps.

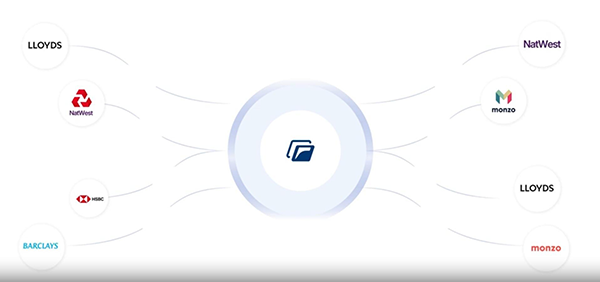

These providers offer unified API layers combining both AIS and PIS capabilities, reducing integration surface area. They provide agent licensing access to growth-stage platforms, not just enterprises. And they structure pricing to scale with platform growth rather than imposing enterprise minimums.

Finexer is one such provider. Built specifically for growth-stage platforms across accounting, ERP, and vertical SaaS, it provides an open banking API for both bank data access and payment initiation through a single integration.

“We built Finexer after seeing platforms encounter similar integration challenges,” says Ravi Ranjan, CEO of Finexer. “The infrastructure existed, but the delivery model excluded most of the platforms that actually needed it. That gap felt solvable, and we focused on addressing it.”

For accounting platforms, this means moving away from CSV imports toward live bank transaction feeds, triggering automated reconciliation from payment events, and initiating supplier payments directly through their software, all through a single infrastructure layer.

Deployment typically happens 3x faster than traditional enterprise integrations. Platforms often report integration timelines measured in weeks rather than quarters. Pricing scales with usage rather than imposing fixed commitments.

Infrastructure patterns emerging across the sector

The shift from manual to API-based infrastructure isn’t happening through competitive provider switching. Most growth-stage platforms weren’t using any Open Banking infrastructure at all.

They were dependent on CSV bank statement uploads, manual processes, and traditional payment methods, not because these methods were preferable, but because they represented the only viable path suiting their operational needs.

As infrastructure providers serving growth-stage platforms enter the market, this is changing. Platforms that previously couldn’t justify the cost or complexity of enterprise Open Banking integrations now have alternatives aligned with their scale and speed requirements.

The pattern is consistent: platforms integrate infrastructure, start with basic connectivity, then expand usage as workflows become progressively automated. Real-time transaction feeds replace batch CSV imports. Payment initiation replaces manual bank transfers or high-fee card processing.

Reconciliation moves from month-end manual matching to event-driven automation.

Fun Fact

Older methods required you to provide your bank account details to applications. Open banking uses secure tokens that grant limited, revocable access, meaning the app never sees your credentials.

What this means for accounting software providers

As Open Banking infrastructure becomes accessible at different price points and deployment models, operational capabilities shift.

Real-time financial visibility replaces delayed bank statement imports. Automated reconciliation triggered by live payment events reduces manual data entry and the error rates that come with it.

Payment processing costs can decrease as platforms shift from percentage-based card fees to flat-fee account-to-account transfers.

For SMEs, automated data feeds and real-time reconciliation already deliver an estimated £1.4bn in annual value, highlighting the operational impact of Open Banking-enabled workflows.

For platforms making integration decisions today, the market has changed. The question is no longer whether Open Banking technology is enough. The question is whether the required infrastructure exists that matches your platform’s operational requirements, scale, speed, and budget.

Making Tax Digital adds urgency. MTD Phase 2 requirements for digital tax filing (April 2026) create a clear regulatory deadline. Real-time bank data access via API provides the connectivity required to meet these requirements. Platforms integrating now will be positioned ahead of the deadline.

The infrastructure gap is closing

The adoption of Open Banking in the accounting sector was never limited by demand or technical capability. Accounting platforms understood that value. The technology has proven quite effective in many instances. The regulatory framework was clear.

The limiting factor was access. Open Banking providers were designed with enterprise clients in mind, with pricing and operating models that didn’t translate well to smaller platforms.

That’s changing. Infrastructure providers like Finexer, built specifically for growth-stage platforms, are making bank connectivity accessible at scales that previously couldn’t justify the integration cost or complexity.

For accounting software providers, the question isn’t whether to integrate Open Banking. The question is timing, and which infrastructure model aligns with how your platform operates.

About Finexer

Finexer is an FCA-authorised Open Banking API provider in the UK that enables platforms to access real-time bank data, initiate account-to-account payments, and verify financial information through a single integration. It is used by accounting, ERP, and fintech platforms to automate reconciliation, replace manual bank data collection, and build real-time financial workflows.

Book a demo to see how Finexer integrates with your Accounting platform!

Author - Shourya Kumar

Finance Writer

Related Posts